June 2026 Vol. 81 No. 6

Features

28th annual horizontal directional drilling survey: Robust HDD growth includes challenges, risks

Robert Carpenter, Editor-in-Chief

As we reach the midway point of 2026, the sometimes mad, occasionally wild, often rewarding and always adventurous roller coaster ride of horizontal directional drilling continues. Demand for HDD’s minimally invasive, environmentally friendly method of installing underground utilities and pipelines is maintaining its robust growth through the first half of 2026, with all signs pointing to a thriving market through the end of the decade.

For more than 28 years, Underground Infrastructure has been conducting research into the unique technology and applications of HDD and its impacts upon the utility and pipeline markets. This research focuses on the U.S. market, which accounts for approximately 36 percent of worldwide applications.

This research effort was conducted during March, April and early May of 2026. It polled U.S. contractors that actively own and operate HDD units to enable a statistical portrayal of the market, from small rigs to large and jumbo models. While comprising only a tiny fraction of the overall HDD work, included in the survey are municipalities and utilities that actually own and operate rigs.

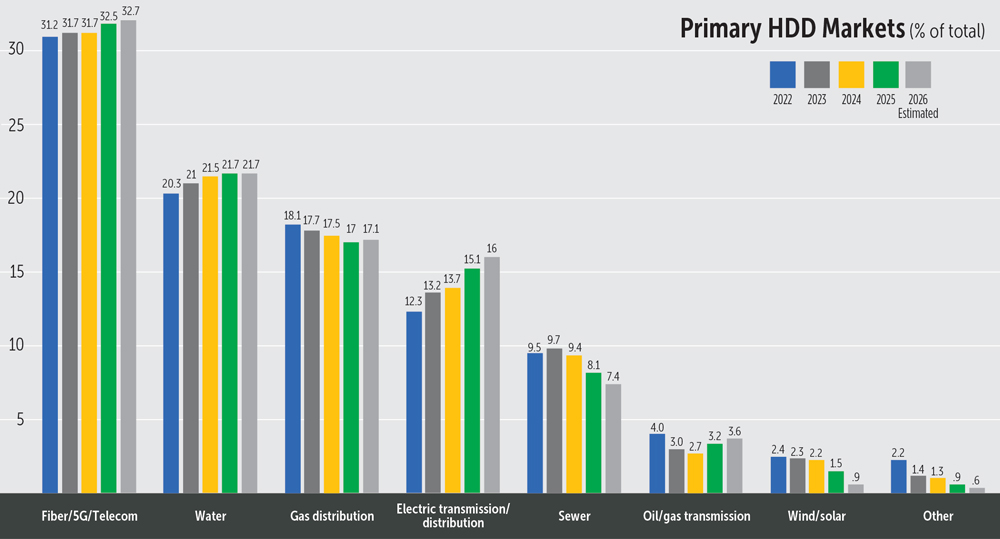

In 2026, the primary HDD markets are fiber/5G, with a 32.7 percent market share and water at 21.7 percent share. Gas distribution declined to 16.0 percent, electric work grew to 17.1 percent, sewer fell to 7.4 percent, oil and gas transmission pipeline work will grow to 3.6 percent, while wind and solar work fell to about .9 percent of the market. Keep in mind that sometimes these market breakdowns are misleading. While a market segment may be accounting for a smaller percentage of work than in 2025, actual work may be higher due to the robust increases in overall market demands.

Market confidence and excitement highlighted the responses to this survey. “We’ve buying another rig for the summer construction season,” said this contractor from the New England region. “Our work just hasn’t slowed down; it’s speeding up.”

“We’re committed for a year,” said this fiber/electric contractor from the Southwest about its scheduled workload. “If we can find additional good help, we’re prepared to add two more rigs to our fleet.”

LEARNING FROM THE PAST

But there are concerns for an industry operating at this growth rate, especially for all the new entrants into the market arena. Not unlike the 1990s through 2020, the first fiber boom also saw the small rig market expand exponentially – always on the cusp of being out of control – and there are corollary problems emerging in the overall HDD market today. Lack of experience can lead to shaky business cultures including poor bidding practices and most importantly, unsafe operational practices resulting in damage to underground utilities that can lead to localize bans on drilling.

“The market is solid,” said this veteran Southwest contractor. “But we’ve got a lot of challenges ahead of us.”

Fortunately, the Horizontal Directional Drilling Association (HDDA) recognizes the opportunities coupled with the needs and risks of this powerful technology that has forever changed the way underground infrastructure is installed. The fast-growing HDDA is actively developing in-depth online training modules focused on many of these critical functions and concerns of modern HDD applications. The program is expected to launch later in the year and is expected to play a key role in stabilizing and professionalizing the HDD industry.

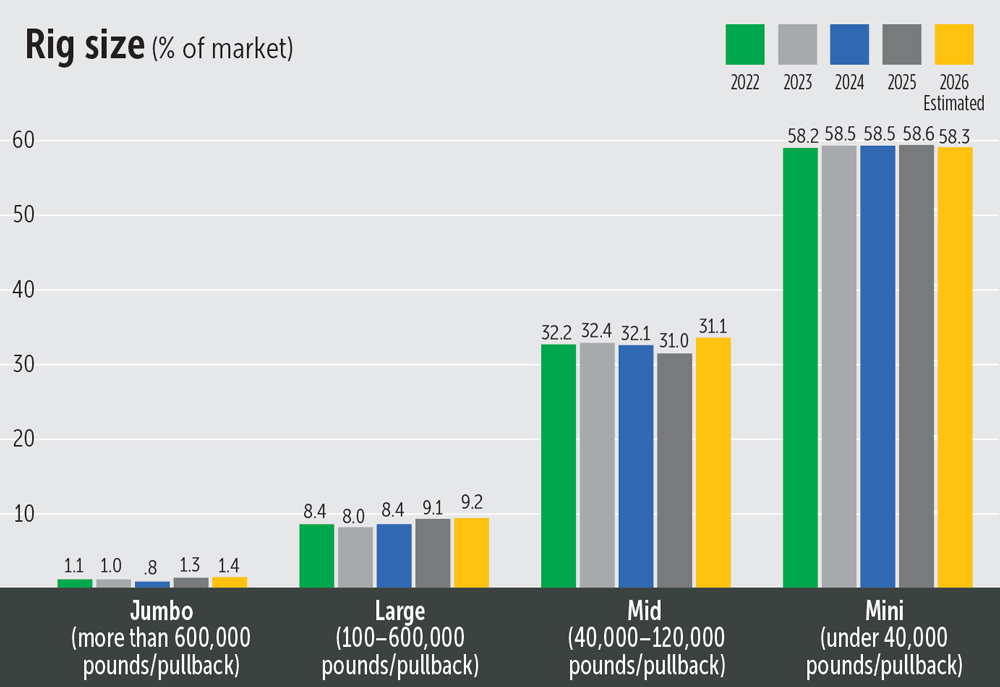

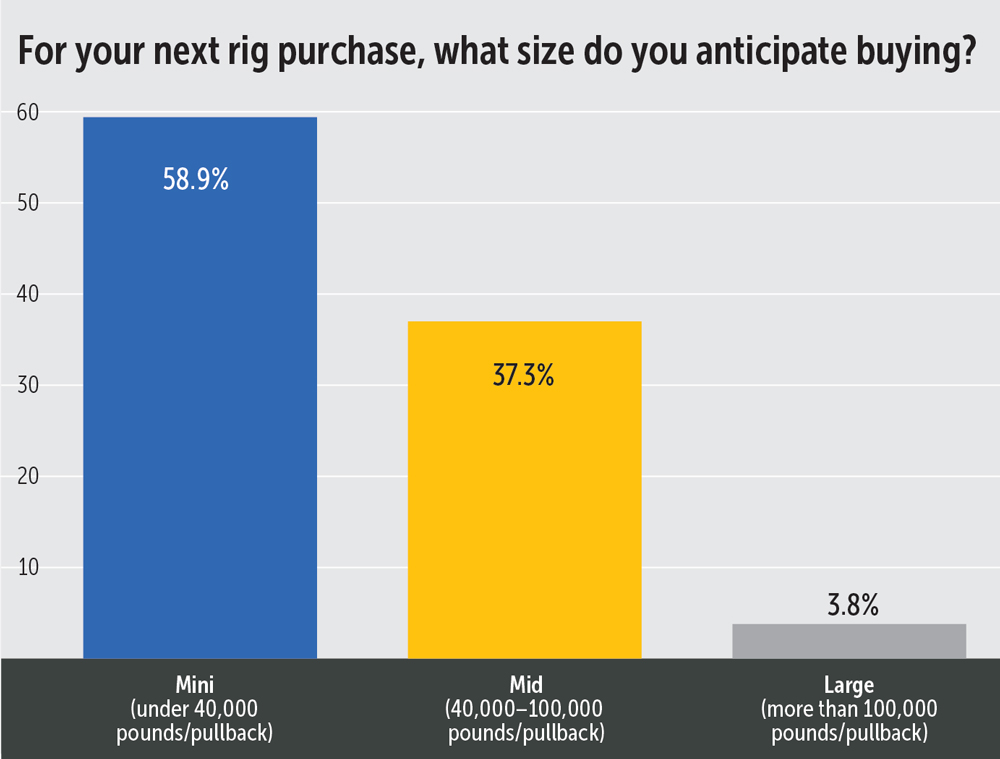

When it comes to buying new rigs, an interesting twist came from a question related to what size rigs contractors were planning for their next purchase. As expected, small rigs dominated at 58.9 percent. But that is down from a 59.4 percent market share in 2025. The twist is that more small rigs will be purchased in 2026 due to the increase in overall rigs sales; but, as a representative total number, the market share of small rig purchases is less.

Medium-sized rigs climbed from 37 percent in 2025 to 37.3 in 2026 and large rigs (greater than 100,000 pounds of pullback) should see their market share climb to 3.8 percent, up from 3.6 percent last year. It is a minor percentage change, but costs involved in owning and operating/equipping medium and large rigs are dramatically higher than smaller drilling units.

Rig manufacturing has been back on the growth track since COVID peaked, and 2026 is expected to be a very strong year. While overall product demands combined with tariffs for certain materials, have tightened some supply lines, overall, there is minimal slowdown in delivery. One manufacturer recently advised that to avoid any delays, the sooner a contractor can commit to a new rig purchase, the better. Rigs, along with ancillary equipment and popular tooling, can sometimes experience delays in delivery.

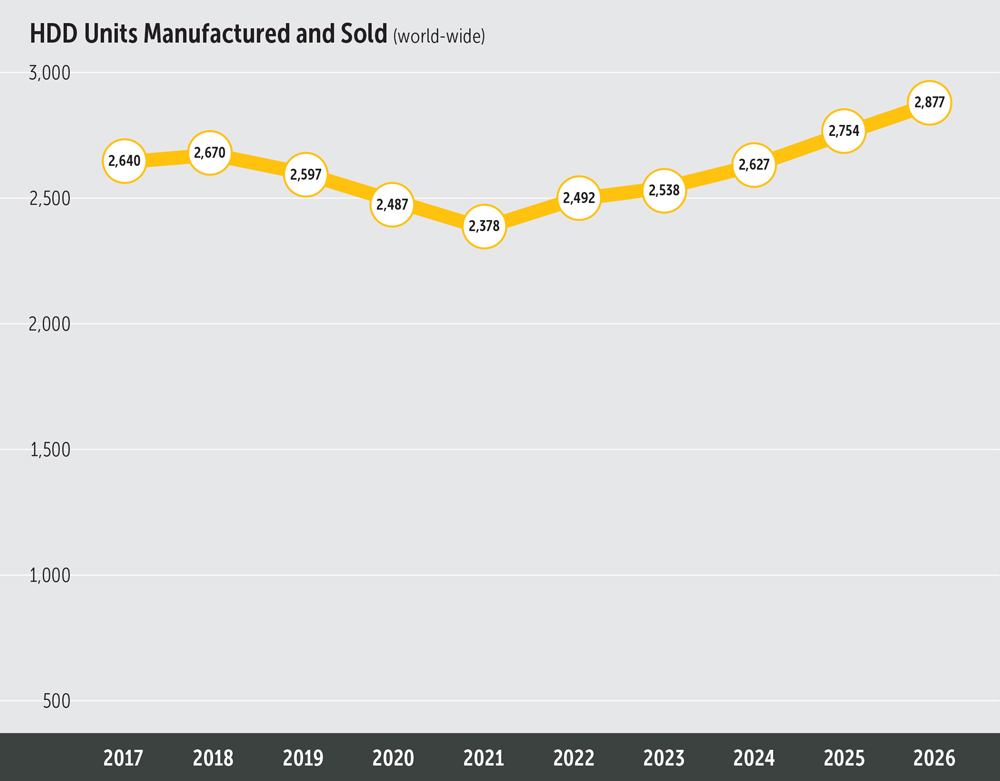

The robust nature of the American utility and pipeline markets is seen in the manufacturing growth of HDD rigs (all size categories). In 2025, the world’s rig manufacturers produced roughly 2,750 units – the largest number since the height of the first fiber boom in 2020. Now, in 2026, rig sales are predicted to top 2,877 units or an increase of 4.3 percent.

MORE GROWTH EXPECTED

The well-documented fiber optic-to-the-home and/or -premises have been primarily driving the small rig market for several years. However, four new wrinkles started feeding additional business development in 2025 and, in 2026, those factors have steered the HDD engine into considerable diverse growth across all HDD markets: BEAD (for fiber related work), electric hardening, data centers and pipelines.

The Broadband Equity, Access and Deployment (BEAD) portion of the famous 2021 Infrastructure Act, after much red tape and several bureaucratic stumbles, has arrived with $42.45 billion in funding. It is a federal program aimed at closing the digital divide by providing high-speed internet access across the United States, particularly in rural and unserved areas, thus ensuring that every American has access to reliable internet.

Federal funding is always welcome but rarely expected. For now, the fiber optic market has become a self-sustaining boom market, thanks to the country’s insatiable hunger for the speed, accessibility and bandwidth that only fiber can provide. Combined with advances in artificial intelligence (AI) and resulting data center construction, demand for fiber installation just keeps climbing. For the next few years, the billions in BEAD funding may be slowed in being digested into the construction market.

Another reason there may be a less-than-enthusiastic response by many contractors to BEAD contracts is the fact that power companies have already accelerated their market expansion, also with billions from the Infrastructure Act. HDD plays not only a key role in power installation, but an increasingly larger role, as well. The goal is to aid power companies in “hardening” (weather proofing) their power lines from foul weather such as hurricanes, tornadoes, ice, wind, lightening, snowstorms, flooding, etc.

While there are several methods to accomplish this hardening, the generally accepted and increasingly preferred method – both by utilities and state and local governing entities – is to place their power lines underground. This means HDD is now being asked to play a significant role in both the relocation and new installation of power lines. Subsequently, there is a major uptick in using HDD to place distribution lines – and even the more complicated and expensive transmission power lines – underground. HDD is the fastest, simplest and most effective way of moving power lines out of Mother Nature’s wrath.

The AI explosion and immediate need for massive data centers to accommodate sophisticated servers has generated a heretofore unheard of demand for utility services. Fiber, electricity, power and water are all essential for data centers. Power to supply electricity is primarily coming from gas so pipeline work is needed. Further, water is essential to help with cooling systems for the tremendous heat generated by data centers.

Numerous data centers have been announced and are in the planning stages, with more facilities being explored. The great unknown is just how many data centers are actually needed both now and, in the future, and how many have the financing in place to build and operate those centers. Right now, AI is growing exponentially so the data center market remains essentially a new frontier for utility construction.

After several years of slumbering, energy pipelines have awakened. The opening of the LNG export markets is driving much of the work. But increased demand from data center construction is forcing gas companies to re-evaluate their capacities. Many are adding to their infrastructure to handle anticipated needs as this market is just beginning to hit its stride. These developments have led to strong pipeline construction, primarily for natural gas, in 2026 and many additional projects hustling to gain approval before the end of President Trump’s term.

All that bodes well for the large rig HDD market.

PIPE TYPES

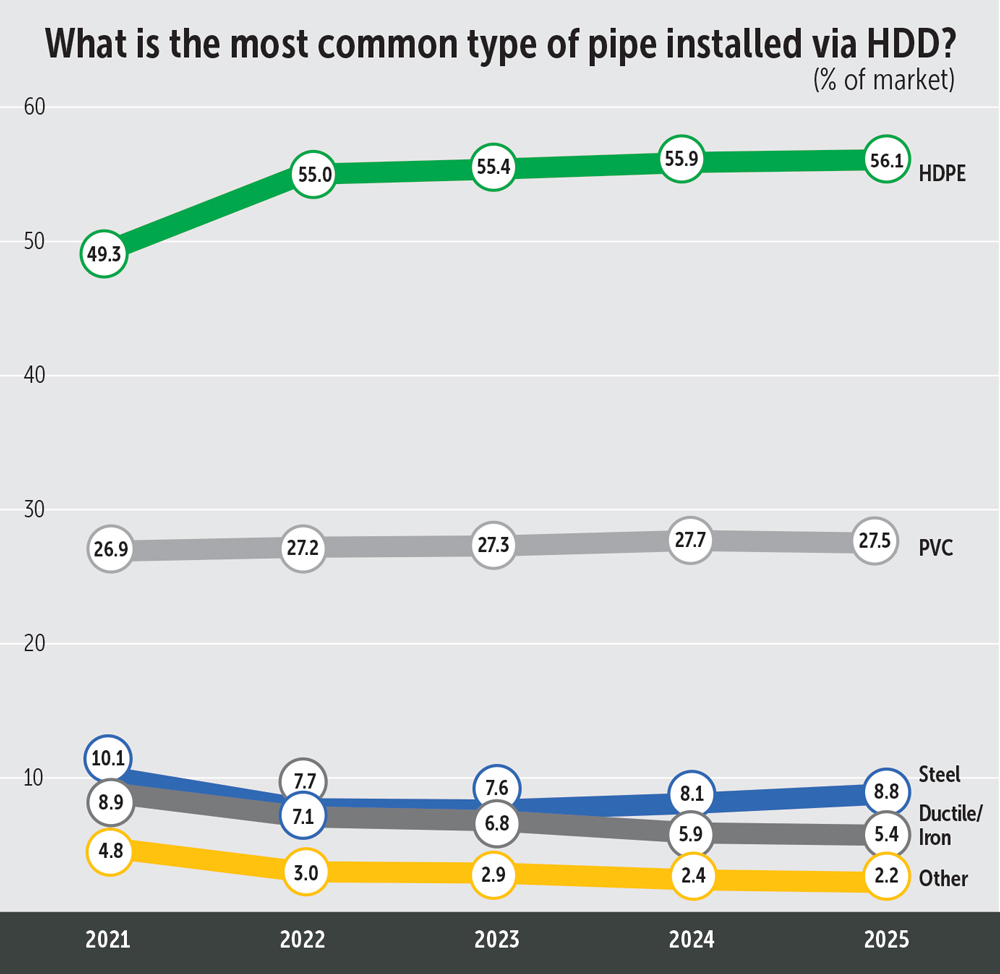

In terms of the most common type of pipe used for installation, high-density polyethylene (HDPE) pipe continues to be the most popular choice for a variety of reasons and saw its market share increase slightly from 55.9 percent in 2024, to 56.1 percent in 2025. Polyvinyl chloride (PVC) pipe remains firmly entrenched as the second-most installed pipe at 27.5 percent, while steel comprised 8.8 percent of pipe used. With the renewed use of steel via energy pipeline growth, steel should see its share of the market increase over the next two years.

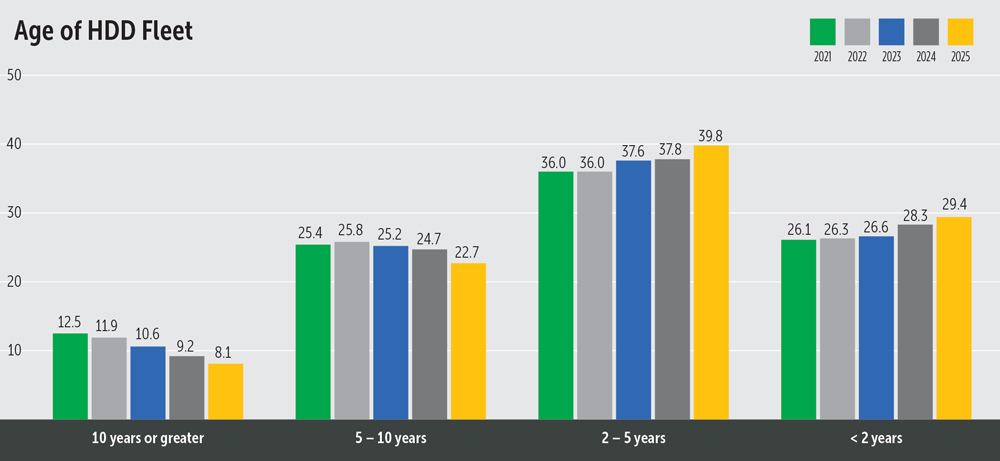

The overall rig fleet continues its youth trend. Older rigs are being worked hard and subsequentially retired and replaced with newer models. Also, especially in the small and mid-sized rig markets, the technology of the newer rigs offers more productivity and a quicker training curve for younger and inexperienced personnel. Contractors are, therefore, motivated to move quickly into newer units by the practicality of busy market conditions combined with an expanding workforce.

Rigs more than 10 years old comprise 8.1 percent of the market, down from 9.2 percent in 2024; 22.7 percent are five to 10 years of age; 39.2 percent are two to five years old; and 29.4 percent of active rigs are less than two years old.

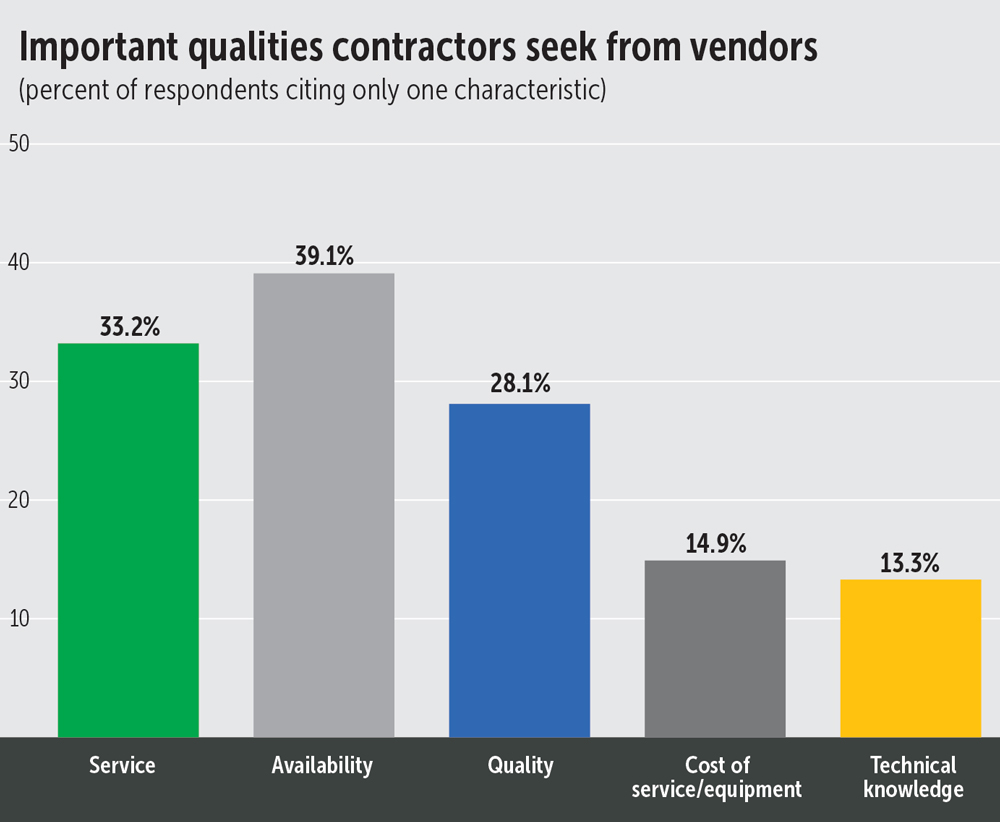

The survey historically asks contractors about the most important characteristics and needs they seek from their manufacturer and supplier partners. For 2026, availability/field support of equipment was cited by 39.1 percent of contractors, up from 36.2 percent in 2025. Service remained a strong desirable characteristic from vendors, as noted by 33.2 percent of the survey respondents. Quality was in third place but jumped from 22.0 percent in 2025 to 28.1 percent in 2026. Next was cost of service/equipment at 14.9 percent and technical knowledge at 13.3 percent.

A question added to the survey this year related to how vendors/manufacturers can attune to the often immense, broad and immediate needs of contractors, especially for those smaller rig contractors working in the fiber and electric industries. Quick response times and fast mobilization are always critical. How vendors, dealers and manufacturers are able to accommodate the high demands of their customers cannot be taken for granted, especially in an increasingly highly competitive HDD marketplace.

As a whole, most of the veteran contractors have long-established ties with dealers/suppliers and on a scale of 1 (poor) to 5 (excellent), vendors receive a solid score of 4.1.

“We’ve been in business since the 90s, through boom-and-bust times, and our suppliers have always stepped up and help us through challenges,” observed this Southwest contractor. “Couldn’t have made it to where we are today without their help.”

On the other hand, newer contractors, especially in the small rig markets, are struggling to meet the needs and expectations of a hectic industry.

“We’ve only been in the market for a couple of years,” said this West Coast contractor. “We’re definitely on a steep learning curve. We’ve had some valuable help from our suppliers, as a whole, but we also get the feeling like we’re a nuisance to other vendors that are swamped with established customers. I can understand that to a degree, but we’re building a company here and sometimes we have to be the squeaky wheel,” he pointed out.

Comments